With the midterms, ‘who won’ is the smaller question

Consumers want affordability; for corporations, the concern is consistency

5 min read

KEY POINTS

- Rising costs remain a top concern for many Americans, making affordability a key issue as voters head to the polls.

- Businesses are making major long-term investments in AI, infrastructure and manufacturing, but many decisions depend on a stable and predictable policy environment.

- As companies rethink global supply chains and invest closer to home, consistent policies may play a greater role in economic growth than any single election outcome.

With U.S. midterm elections on the horizon, the question isn’t just which party wins. It’s also whether consumers and businesses feel confident enough that the current affordability issues will subside and whether policies remain consistent enough for businesses to make long-term decisions.

That distinction is becoming increasingly important in today’s economic environment. While elections can shift priorities quickly, many of the forces shaping growth—capital investment, supply chain realignment and the development of artificial intelligence (AI)—are unfolding over years, not election cycles. That disconnect between short-term political change and long-term economic strategy is beginning to influence how businesses and investors think about risk, while for many consumers, price concerns are paramount.

As BOK Financial® Chief Investment Officer Brian Henderson noted, economic conditions, not just politics, are already shaping the conversation—and high prices are at the top of many people’s minds.

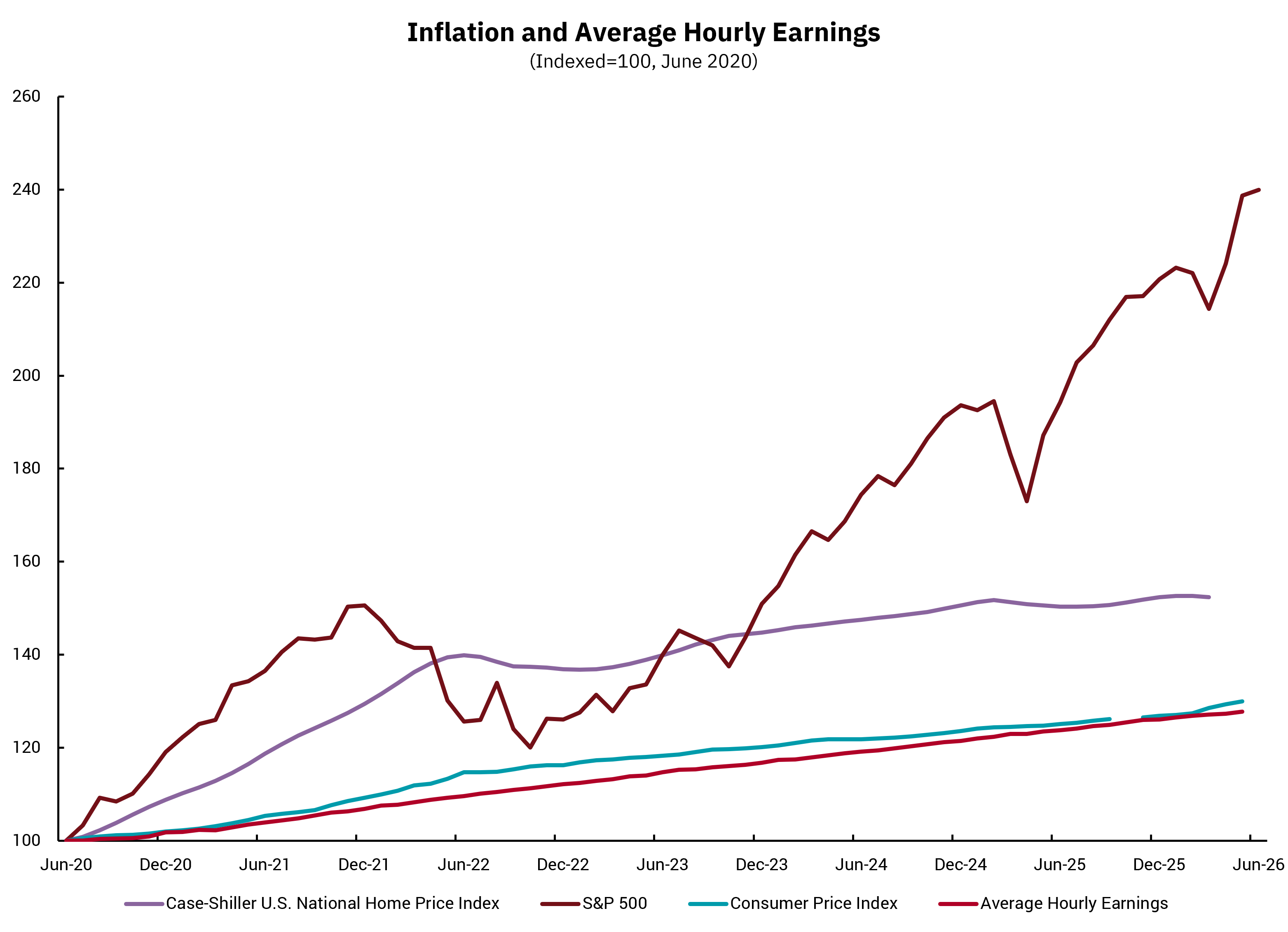

“Affordability is still an issue for the average American,” he said, pointing to the ongoing cost-of-living pressures that continue to weigh on households. These pressures tend to weigh on lower-income households the most, due to aggregate inflation exceeding aggregate wage gains since 2020, according to the Bureau of Labor Statistics data.

Higher-income individuals have been less stressed by aggregate inflation and those with financial assets actually have benefitted during the period, resulting in what some are calling a “K-shaped” economic recovery.

Source: U.S. Bureau of Labor Statistics via FRED®. Data as of June 2026.

Since the top 10% of income earners in the U.S. are responsible for roughly half of all consumer spending, U.S. gross domestic product (GDP) is still growing, despite the affordability issues many Americans are feeling.

However, while GDP might not reflect this strain, the midterm results just might, resulting in a potential shift in Congressional control, Henderson said.

Policy consistency is key to capex

Behind the election cycle, the U.S. economy is undergoing a significant shift, driven by rising levels of capital investment. As BOK Financial Chief Investment Strategist Steve Wyett explained, “We’re in a capital expenditure [capex] cycle that’s being driven by major structural forces—artificial intelligence [AI], manufacturing and infrastructure. It’s the biggest capital expenditure environment for businesses since the railroads.”

Recent tax policy changes have reinforced this trend by allowing companies to more quickly recover the cost of investments in equipment, facilities and research. That effectively lowers the cost of capital and improves cash flow, giving businesses an added incentive to move forward with large-scale projects. In many cases, these incentives are front-loaded, encouraging companies to invest sooner rather than later.

These investments are designed to span years, not election cycles, which means that policy consistency is a major question for the corporations making those capex decisions. “The whole purpose of making a capital investment is so that a business can get a productivity benefit out of making this investment,” explained Matt Stephani, president of Cavanal Hill Investment Management Inc.

However, that productivity benefit depends on a stable policy environment, he noted. If the policies that support investment—such as tax incentives, trade structures and regulatory frameworks—are vulnerable to reversal every two years, companies may delay decisions, scale back investment or redirect capital to areas with greater certainty, he explained.

Deglobalization raises the stakes

This policy uncertainty is unfolding at the same time as a broader structural shift in the global economy—deglobalization, which is causing countries and corporations to rethink supply chains, prioritizing reliability and security over cost. “Companies can’t just rely anymore on where production and labor are the cheapest,” Stephani said.

As part of that shift, some U.S. corporations are choosing to manufacture domestically and some non-U.S. companies are developing production in the U.S., Stephani said. This investment in production can help the companies avoid tariffs or supply disruptions, and in some cases, be “almost deflationary” by reducing reliance on imports, he explained.

The challenge is that these benefits take time—and depend on consistent policy support, which can vary in the U.S. election cycle.

Investment depends on follow-through

At the same time, the U.S. economy is being increasingly driven by capital investment rather than consumer spending, which means that long-term planning is key for politicians and business leaders alike.

In practical terms, this means that today’s policy decisions are setting the foundation for economic outcomes down the road. Projects like manufacturing facilities, energy infrastructure and data centers require significant upfront capital and long development timelines, making consistency a critical factor in whether those investments move forward.

And so, while midterm elections are inherently short-term events, the economic shifts underway—deglobalization, supply-chain restructuring and capex investment in productivity—are playing out over much longer timelines. This means that the real risk isn’t a single election outcome, it’s whether there is confidence in policy consistency, experts agreed.

Read more of our 2026 Midyear Market Update.