Jobs growth continues to hold up

Recent job gains and broader market signals suggest the underlying momentum remains intact amid rising risks

5 min read

KEY POINTS

- Job growth has slowed significantly since 2023, but recent months have outperformed expectations, signaling underlying economic strength.

- Policy support, corporate earnings and investment trends are helping to sustain momentum despite geopolitical and inflationary risks.

- Shifts in the size of the labor force mean that fewer jobs are needed to maintain low unemployment, easing fears of a sharp downturn in consumer activity.

The monthly report from the Bureau of Labor Statistics (BLS) is arguably the single most important data out there, as it pertains to the outlook for the U.S. economy. With consumer spending making up two-thirds of U.S. annual gross domestic product (GDP), having a job is a key determinant of the direction of spending. In addition, full employment is one of the two mandates for the Federal Reserve, so the health of the job market plays a vital role in forecasting the future of monetary policy too.

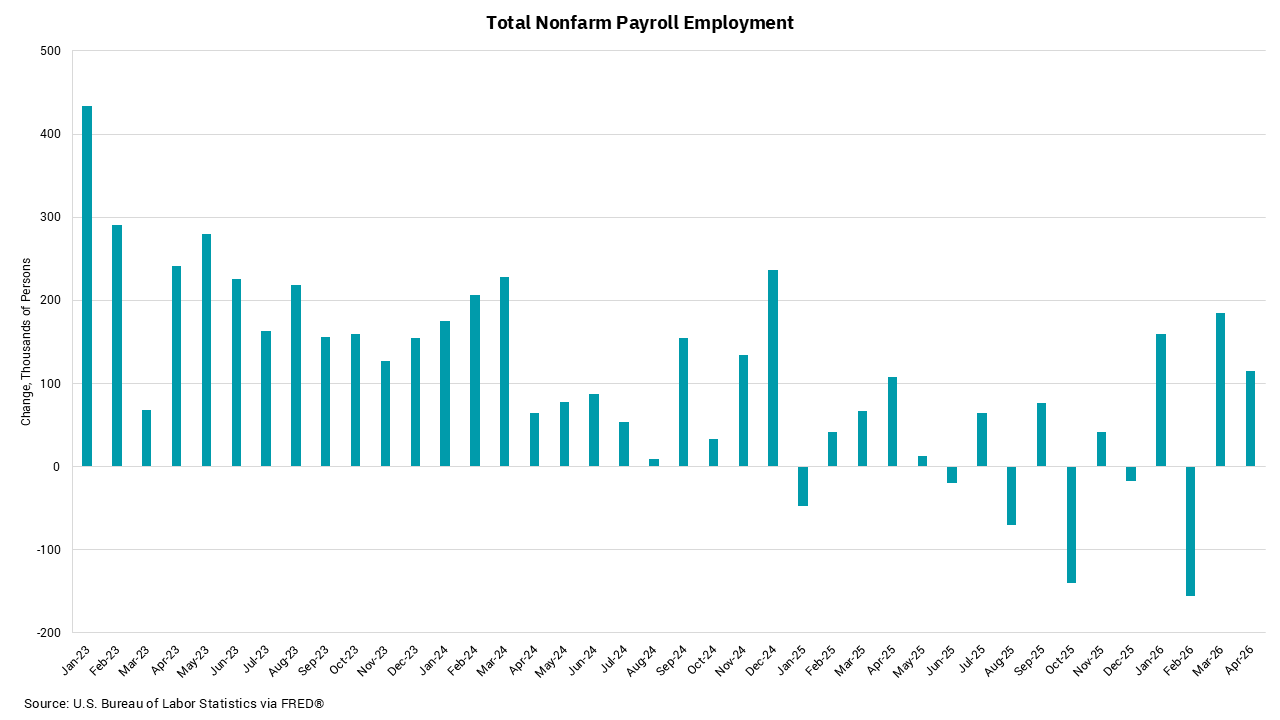

There are multiple data points within the report to consider—including readings on wage inflation, the level of participation in the labor force, data on hours, the headline unemployment rate (U3) and the “underemployed” rate (U6). This week’s chart shows another very important part of the report—the number of new jobs created, or “nonfarm employment” growth. We looked at data going back to 2023 to try and get an idea of the trend we are seeing. Doing so, it’s clear that overall job growth has been slowing. Average monthly job growth near 175,000 in 2023 is now only about 50,000 with multiple months since January 2025 showing negative job growth.

The last two months are particularly interesting. We have been amid the Iran conflict during this period, and yet in both months, new job growth has exceeded both the recent average, and expectations. Based on consumer sentiment surveys and spikes in gasoline prices, one might have expected hiring to slow as the economic outlook became cloudier. Instead, the cumulative effect of Fed rate cuts over the last 24 months, incentives in the passage of the One Big Beautiful Bill Act for both consumers and especially businesses, the ongoing AI capex super-cycle, healthy first quarter corporate earnings and increasing earnings expectations for the remainder of 2026 and into 2027 have all led to a series of record highs in the major domestic stock averages and increasing.

However, this is not to say that risks are not evident. A longer duration to the conflict in Iran may lead to higher inflation and structurally higher energy prices which would pressure consumers. Still, the underlying momentum in the U.S. economy is positive. We have also begun to see an expansion of expected earnings growth beyond the “Mag 7” to include a broader swath of companies in the mid-cap and small-cap arenas. In fact, since the outbreak of the conflict, small-cap stocks have outperformed large-cap stocks, which is a strong message from the market that the conflict is expected to be resolved and reduce headwinds to growth going forward.

At the same time, it is true that we are seeing changes to both the numerator and the denominator of the unemployment calculation. As our labor force shrinks in size, primarily due to retirements but also due to changes in immigration policies, it takes fewer new jobs to keep the unemployment rate steady. However, this month’s data helps reduce fears of a spike in unemployment that would lead to a decline in consumer-led economic activity.

Get By the Numbers delivered to your inbox.

Subscribe (Opens in a new tab)